Wall Street has once again confused momentum with immortality.

If you had opened a respectable financial magazine in 1980 and searched for the greatest places to preserve wealth during the previous decade, the U.S. stock market would have appeared somewhere between “used carpeting” and “Soviet agricultural equipment.”

That surprises modern investors because today people speak about stocks the way medieval peasants spoke about holy relics — with trembling devotion and absolutely no understanding of the underlying mechanics.

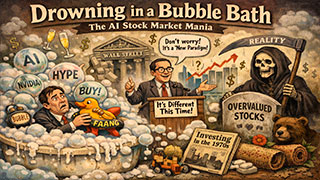

But the 1970s were not kind to equity investors. Not dramatic, not cinematic, not even particularly loud. The crash of 1929 felt like being thrown from the roof of a 60-story building. The decline of the 1970s was slower, gentler, and somehow crueler. It was more like being slowly drowned in a bubble bath while economists reassured you the water temperature remained historically supportive.

By the end of the decade, investors had lost roughly half their purchasing power, though many remained cheerful because their brokers kept using phrases like “long-term secular opportunity.”

Now here we are again.

Different decade.

Different buzzwords.

Same perfume on the same corpse.

Today the market has discovered Artificial Intelligence, which is fortunate, because until recently investors were running out of excuses to justify paying forty times earnings for companies whose primary business activity appears to be announcing partnerships with each other.

The concentration alone should make sensible people nervous, which is precisely why nobody on Wall Street is nervous.

In the late 1960s, investors worshipped the “Nifty Fifty,” a collection of untouchable growth companies that people believed could be purchased at any price because America itself would sooner stop breathing than allow those stocks to fall. Then came the 1970s, which introduced investors to the exciting new concept that even magnificent companies can become terrible investments if bought at idiotic prices.

In 2000, technology and telecom stocks ballooned to roughly 41% of the market. Analysts insisted the internet had permanently eliminated recessions, valuation concerns, and apparently gravity itself. Then the Nasdaq collapsed with such force that grown men began pretending they had always preferred bonds.

Today Big AI once again accounts for roughly 41% of the S&P 500. History does not repeat itself, but it does enjoy wearing the same hat to different funerals.

The modern investor has become a remarkable creature. He no longer buys earnings. Earnings are old-fashioned. Earnings are for accountants, undertakers, and people who read footnotes voluntarily. Today’s investor buys acceleration. He buys narrative. He buys the possibility that another investor, even less sober than himself, might arrive tomorrow willing to pay an even more ridiculous price.

Price-to-earnings ratios are now treated the way children treat vegetables: technically important, but best ignored until absolutely necessary.

Take NVIDIA, the patron saint of AI speculation. The company is extraordinary. Its products are extraordinary. Its profitability is extraordinary. And its valuation occasionally resembles the final moments of a gold rush where prospectors have started selling imaginary shovels to one another.

Meanwhile, investors have stopped caring about beta altogether.

For reference:

Beta is a widely used indicator of a stock’s price volatility or the level of risk relative to the broader market.

Once upon a time, a high beta stock meant elevated volatility and greater risk. Today it simply means the stock can ruin your emotional stability at a higher speed.

People no longer ask, “How much does this company earn per share?”

They ask, “Can this thing double before reality notices?”

And reality, to be fair, is often late to the party. Sometimes very late. In speculative markets, absurdity can remain fashionable far longer than prudence can remain solvent.

To make matters worse, corporate earnings are actually strong right now, which is exactly the sort of detail that gives bubbles their dangerous credibility. The late 1960s had good earnings too. So did 2000. Investors always assume bubbles are accompanied by terrible fundamentals, but genuine bubbles usually emerge from excellent businesses wrapped in catastrophic levels of enthusiasm.

That is what makes them seductive.

No investor ever says, “I am participating in an unsustainable mania fueled by liquidity, ego, and professional jealousy.”

Instead they say things like, “This technological paradigm shift justifies premium multiples.”

Which is Wall Street’s elegant way of saying, “I know this is insane, but everyone else is making money.”

And perhaps the optimists will be right. Perhaps AI truly will reshape civilization, automate labor, transform productivity, cure disease, write novels, manage portfolios, and eventually explain to investors why they paid 43 timesfor a company selling expensive calculators to data centers.

Andrievskii Verdict:

This rally could last another five years, or it could end tomorrow before my coffee gets cold.

But there is something deeply unsettling about a market where valuation metrics are increasingly viewed as emotional negativity, caution is treated like intellectual failure, and buying momentum has become a substitute for having an investment thesis.

At some point, the market stops weighing value and starts acting like a lottery ticket printed by MBAs. This phase can last way longer than you think, right until the bubble foam fills your lungs.

Aleksei Andrievskii is the founder of the ANDRIEVSKII SEA WEALTH family office in Cyprus, a member of the advisory board at Bendura Bank AG, Liechtenstein